If you’ve ever wondered how to keep your spending under control without getting into complicated spreadsheets, the 50/30/20 budget rule is a pretty handy way to start. It’s a simple rule of thumb that can help you organize your money in a way that feels balanced, instead of restrictive. I first heard about this method years ago when my own budget felt totally out of control, and it honestly took a lot of stress off my shoulders. Here’s what makes this rule popular, who gets the most out of using it, and exactly how it works in real life.

Why the 50/30/20 Rule Is So Popular

This budget method pops up just about everywhere, especially in beginner finance guides. It’s easy to see why. The rule cuts right through all the drama and gives you three clear places for your money. You don’t need special apps or a finance background to use it, and you won’t find yourself tracking every single coffee or splurge. When I recommend this method to friends who feel overwhelmed, they usually say it’s the first system that actually feels doable for them.

It’s popular because it’s less about making you feel guilty and more about helping you understand where your money is actually going. The simplicity makes sticking to a budget less like a chore and more like a regular habit.

Who Benefits Most From This Rule?

Anyone can use the 50/30/20 rule, but it’s especially practical for people who have a steady income and want a big-picture way to manage their expenses. If you’re paid the same amount every month and your bills are pretty predictable, this system lines up well with your lifestyle. It works for individuals, couples, and even families who want to get a handle on spending without stress.

If your finances tend to swing up and down (like freelancers or those with irregular hours), it still works, just with a bit of tweaking and tracking. And for those just starting out with budgeting, it offers clear guidelines without a ton of work. In today’s world where expenses seem to keep jumping, families especially can find comfort in this method because it acts as a built-in guardrail instead of an intricate checklist. Even couples merging finances for the first time find the structure gives everyone a sense of control, not limitation. If you ever feel your budget gets off track after big changes (like a new job, a move, or growing your family), it’s relatively easy to recalibrate with this method compared to a super detailed spreadsheet system.

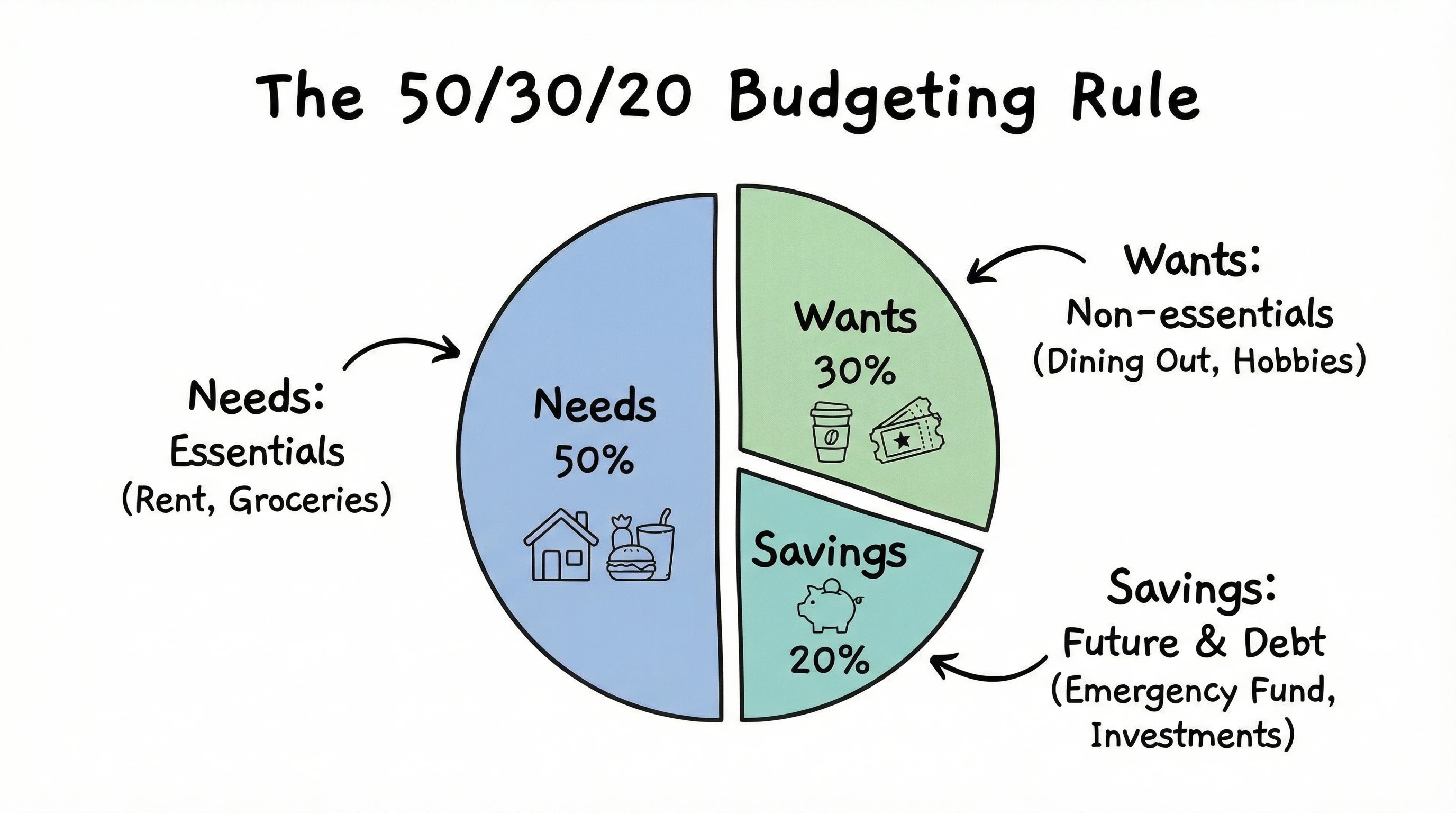

What Is the 50/30/20 Budget Rule?

The core idea is pretty straightforward: split your after-tax income into three easy buckets—needs, wants, and savings or debt repayment. Each gets a percentage of your income, which makes decisions a lot simpler. Here’s how it breaks down:

Needs (50%)

Half of your takehome pay goes to what you really can’t do without. That means things like rent or mortgage, utilities, groceries, insurance, transportation, and minimum debt payments. These are basic things that keep your life running.

If you’re not sure what belongs here, I usually say: if skipping it puts you in a tough spot (like not paying for electricity or missing a student loan payment), it’s probably a need. Remember needs aren’t about just surviving—they’re the essential pieces for stability. For example, safe transportation might mean a bus pass or car insurance, while basic groceries and a reasonable phone plan fall into this group too. It’s also smart to reevaluate what’s truly necessary every so often, especially when expenses or priorities change.

Wants (30%)

This is where you get to enjoy your money without feeling bad. It covers things like your phone upgrade, streaming services, eating out, new clothes, travel, and hobbies. Wants are all those extras that make life fun but aren’t totally necessary.

I found that putting wants in their own category actually helps you spot what you value most. When you give yourself clear permission to spend on fun stuff (within a limit), you’re less likely to overspend overall. Over time, you might notice your personal list of wants changes—a new season could bring new hobbies or interests. The key is to check in with yourself about which extras still feel worthwhile, and which might be costing you more than they’re worth.

Savings (20%)

The last chunk goes to future you. This can mean padding your savings account, building an emergency fund, investing, or making extra payments on loans. If you’re paying off a credit card or student debt above the minimum, that extra can go here too.

I like to set up automatic transfers right after payday. That way, saving just happens without much thought. Consistency, even with smaller amounts, adds up over time. You can also use this part of your budget for financial goals, like saving for a home down payment or planning for a big trip. Many people find that having a labeled goal (like “Vacation Fund” or “Car Repairs”) makes it easier to leave those savings untapped until they’re really needed.

Applying the 50/30/20 Rule Step by Step

Sticking to the 50/30/20 rule doesn’t take a ton of prep, but a little time upfront pays off. Here’s how I’d walk someone through it:

- Calculate Your After-Tax Income: Figure out your monthly income after taxes. That’s your starting point. Don’t forget to factor in any regular side income or freelance money, too. If your income varies, go with a monthly average from the past year. It helps to pull out a few months of bank statements so you’re working with real numbers.

- List Your Expenses: Write down everything you spend in a month. Don’t worry about being perfect at first, it gets easier the more you track it. Some people like to use budgeting apps, but a notepad or phone spreadsheet works just fine. The key is being honest with yourself—even the small recurring charges add up.

- Categorize Each Expense: Group your spending into needs, wants, and savings (or debt payments). This step can be a bit eyeopening, especially if you haven’t tracked before. Some expenses blur the line (like cell phone plans), so just use your best guess and stay consistent. Over time, your gut feeling about which expense goes where will get sharper.

- Compare Against the 50/30/20 Targets: Check out how your spending lines up with the targets. If you’re way off in one area, just adjust the next month; small steps are totally fine. You might start by trimming a few wants or shifting savings goals until everything feels more balanced.

For a more detailed breakdown, check out my full guide on how to create a monthly budget. Creating a budget for the first time is like learning to ride a bike—you might wobble at first, but the process gets smoother with practice.

Example of the 50/30/20 Budget

Sometimes seeing numbers in action helps more than just hearing an explanation. Here’s a practical example with round numbers to keep things simple:

If your after-tax monthly income is $3,000, here’s how the rule breaks down:

- Needs (50%): $1,500 for rent, groceries, utilities, insurance, and minimum payments on loans or credit cards.

- Wants (30%): $900 for eating out, entertainment, subscriptions, traveling, and shopping.

- Savings (20%): $600 for savings, investment accounts, emergency fund, and extra debt payments.

You might find some months look a little different (extra travel or a surprise bill), but this method gives a steady guide. Over a few months, reviewing your actual numbers for these categories can help you fine-tune them, and also spot where money leaks might be happening. Maybe you’re spending more on dining out than expected. That’s a chance to game plan meals at home or switch up your subscriptions. Using this simple breakdown, you get more control over where every dollar goes—without having to micro-track it all the time.

Pros and Cons of the 50/30/20 Rule

Every budgeting method has its strong points and some downsides. Here’s how I see it after using this for a while:

- Pro: Super Simple. The biggest perk is how easy this rule is to use. You can keep track on a notepad, phone app, or mentally tally things if you want.

- Pro: Freedom to Spend. Because you allow for wants, you don’t end up feeling deprived, as long as you keep it within 30%.

- Pro: Encourages Saving. With savings baked in, you’re less likely to put it off till “what’s left over.”

- Con: Not Always Flexible. If your rent alone eats up more than 50%, squeezing into the rule can get tricky, especially in big cities or with rising costs.

- Con: Can Feel Restrictive for Some. Those in nontraditional situations (either super low income or really unpredictable months) might struggle to hit these specific percentages.

It’s really about using the rule as a guide instead of a strict requirement. Adjust as your life and income change, and don’t be afraid to bend the percentages if that helps you stay on track. Budgeting is a personal process, and feeling empowered matters more than sticking to the numbers perfectly. If this rule is your gateway to financial confidence, it’s done its job.

When the 50/30/20 Rule Doesn’t Fit

The rule works for a lot of people, but sometimes it just doesn’t fit the way your finances actually look. Here are situations where you might need more flexibility:

- Low Income: If you’re bringing in barely enough to cover rent, making savings 20% might not be realistic. How to Save Money on a Low Income offers some tweaks and alternatives for these situations. Sometimes, focusing on essential expenses and slowly building up a savings habit—even if it’s just $10 a month—can be a huge win.

- High Fixed Costs: Living in a city with soaring rents or lots of required expenses can make the needs category way more than 50%. In these cases, you might give yourself a smaller “wants” budget and look for creative ways to cut costs. It’s also worth shopping around for better deals on insurance, phone plans, or utilities to see if you can free up a little breathing room.

- Irregular Income: Freelancers or those with variable paychecks often do better tracking average monthly income and adjusting the categories as the money comes in. Some months you might be able to save more, while other months staying afloat is the big win.

If you’re dealing with any of these, don’t get discouraged. The point is to use the rule as a baseline, then switch things up so it works for you. Even if your percentages aren’t perfect every month, practicing mindful spending can still improve your financial health overall. Flexibility is what keeps a budget useful, especially during times of change.

Frequently Asked Questions About the 50/30/20 Rule

Does the 50/30/20 rule work if I’m paying off debt?

Yes, the savings category can include extra payments toward debt above the minimum. It helps speed up the payoff process while you still keep funds for needs and wants. Over time, as debts shrink, you can switch more of this money into long-term savings and investments.

What if my needs are way more than 50%?

You can adjust the percentages. Try shrinking your “wants” category first if possible, or look for areas in “needs” where you might be able to save, like insurance or utilities. If cuts aren’t possible, remind yourself that the rule is meant as a blueprint, not a pass-fail test.

How do I handle irregular expenses, like holiday spending?

Set aside a small amount in “savings” each month for these, so when the holidays roll around you already have a cushion to help cover the extra costs. Planning ahead like this can keep you out of credit card debt and ease up stress when those bigger expenses hit.

Can I use apps to help track the 50/30/20 split?

Absolutely, there are several popular budgeting apps that let you set custom categories and show a clear breakdown. But you can also use spreadsheets, or just check your monthly statements and jot down totals for each category regularly. The tracking method matters less than your consistency and honesty with the numbers.

Using the 50/30/20 Rule as a Helpful Guide

The beauty of the 50/30/20 budget rule is how approachable and flexible it is. It gives you a solid starting point, but you’re in control of the details. If you need more in-depth tips on getting your budget off the ground, you can check out my step-by-step guide on creating a monthly budget. The goal isn’t to create stress; it’s to make money management feel a little lighter and a lot more doable, one month at a time. Remember, a simple plan you stick with beats a “perfect” plan you abandon. Small steps add up to bigger confidence—and better finances—over time.